Every claims operation handles two fundamentally different kinds of work. The first is the steady, predictable rhythm of daily property losses – house fires, water leaks, theft, single-vehicle damage events. These come in at a manageable pace, get assigned through standard workflows, and close at a predictable cadence. The second is what happens when a hurricane makes landfall, a hailstorm sweeps across the Midwest, or a wildfire moves through a region overnight.

On the surface, the work looks similar. An adjuster inspects a property, documents damage, and writes a scope. The carrier reviews the file and processes payment. Same workflow, different volume.

In practice, the two are operationally different in almost every meaningful way. And conflating them is one of the most common – and expensive – mistakes a carrier can make when sizing their claims program for the year.

Volume Is the Most Obvious Difference, but Not the Most Important One

A daily claims operation handles a predictable file count week to week. Adjusters know their territories, their workload, and their reporting lines. The work runs on rhythm.

A catastrophe event compresses six months of volume into six weeks, or sometimes into ten days. The total file count isn’t necessarily larger – what changes is the timing curve. Hundreds of inspections need to happen inside a window where the standard workflow simply can’t absorb them. The infrastructure built for predictable intake breaks down when the curve gets that steep.

This is why most carriers that run daily claims well still struggle with CAT events. The operations were designed for a different shape of volume. The CAT claims adjuster who shows up during a hurricane is solving a different equation than the one solving a routine residential file in March.

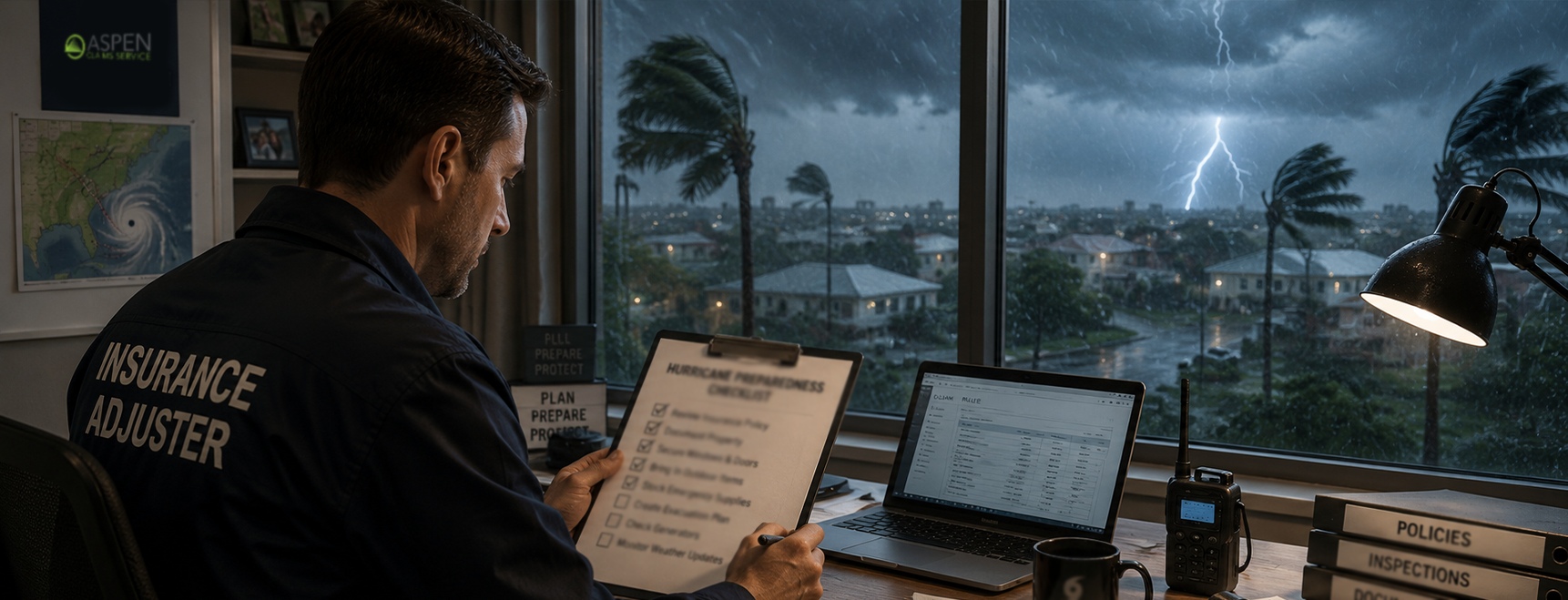

The File Itself Is Different

A daily property claim usually involves one cause of loss, one set of damaged areas, and a relatively contained investigation. The adjuster has time to work the file in sequence – inspection, documentation, scope, review, submission. The pace is steady.

A catastrophe claim sits inside a much messier context. Hurricane files often involve wind versus flood causation disputes, multiple damaged structures on a single property, code upgrade implications, business interruption windows on commercial files, and ALE clocks on residential ones. Hail files involve test square documentation across multiple slopes, soft metal evidence, and increasingly contested causation arguments. Wildfire files involve total loss documentation, contents inventory, and access constraints from active disaster zones.

None of this work is impossible for a daily adjuster. But the volume of detail required per file, combined with the speed required to keep cycle time honest under surge, is what makes catastrophe claims adjusting services structurally different from daily claims handling. The work asks the adjuster to be faster and more careful simultaneously – two operational pressures that usually trade off against each other.

Logistics Become a Competitive Function

Daily claims rarely require complex deployment logistics. An adjuster is assigned, drives to the property, and runs the inspection. The operational support around them is light.

Catastrophe response is a logistics operation as much as it’s a claims operation. Adjusters need to be pre-positioned in affected geographies. Ladder assist resources need to be secured before capacity gets allocated to whoever booked first. Lodging and travel coordination become rate-limiting factors. Field equipment – drones, structural consultants, contents specialists – needs to be lined up before the storm makes landfall, not after.

This is where the independent catastrophe claims adjuster firms that handle CAT well separate from the ones that struggle. The firms with deep CAT logistics infrastructure can move quickly and at scale because the work happened months before the event. The ones treating it as overflow capacity get caught flat-footed.

File Standards Behave Differently Under Surge

This is the part of the difference most people outside the industry underestimate. File standards that hold up at normal volume can degrade quickly during a CAT event. Photo discipline gets thinner. Scope notes get shorter. Coverage documentation becomes a sentence rather than a paragraph. The adjusters aren’t doing worse work – they’re running out of daylight.

The result shows up months later as supplements, reopens, and complaint files. Carriers paying for fast cycle time during the event end up paying again for the documentation gaps once the event has closed. The total cost of the claim turns out to be substantially higher than the initial close suggested.

Catastrophe claims management services that are designed for this environment treat file standards as a non-negotiable input rather than something that flexes under volume. The QA layer doesn’t relax during surge. The photo standards don’t drop. The contemporaneous note expectations don’t shift. This discipline is what separates a CAT response that earns the next deployment from one that doesn’t.

Why the Distinction Matters for Carriers

Most carriers run their claims programs with a single vendor strategy – one set of independent claims adjuster firms handling both daily volume and catastrophe response. It’s simpler to manage and easier to procure. It also produces uneven results during major events, because the operating model required to handle independent adjuster daily claims is genuinely different from the one required to handle a Category 4 hurricane response.

The carriers that perform consistently across both kinds of work usually structure their vendor relationships accordingly – daily capacity built around predictability and territory coverage, CAT capacity built around surge logistics and pre-event readiness. At Aspen, daily and CAT operations are deliberately structured as separate divisions. When the storm hits, daily files keep moving. When daily volume is steady, the CAT bench stays sharp through cross-training and pre-positioned readiness.

Daily and CAT look like the same work. They aren’t. The carriers and vendors that understand the difference are the ones whose policyholders see consistent service whether they file in March or in September.